Home Loan Assistance in Bangalore with Trusted Bank & NBFC Partners

We provide structured home loan assistance in Bangalore with complete documentation support, eligibility assessment, bank coordination, and faster approval processing — from plot purchase to home construction funding.

End-to-End Loan Assistance

✔ Loan eligibility consultation

✔ Documentation & legal coordination

✔ Bank/NBFC partner support

✔ Construction loan guidance

✔ Plot + Home combined funding support

✔ Faster Approvals & Quick TAT

OUR TRUSTED BANKING & FINANCIAL PARTNERS

We are associated with leading financial institutions to offer competitive rates, flexible tenure, and faster approvals.

Simple & Transparent Loan Process

From eligibility check to disbursement — we guide you at every step.

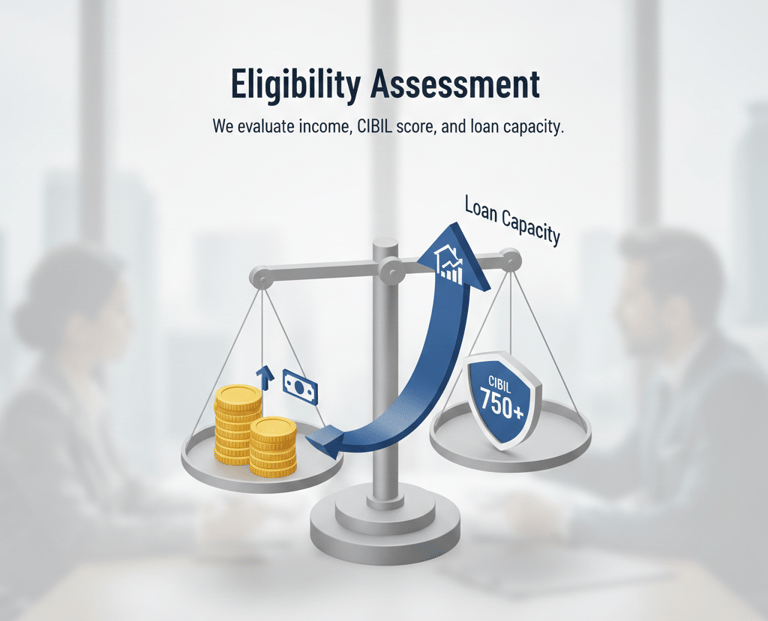

Eligibility Assessment

We evaluate income, CIBIL score, and loan capacity.

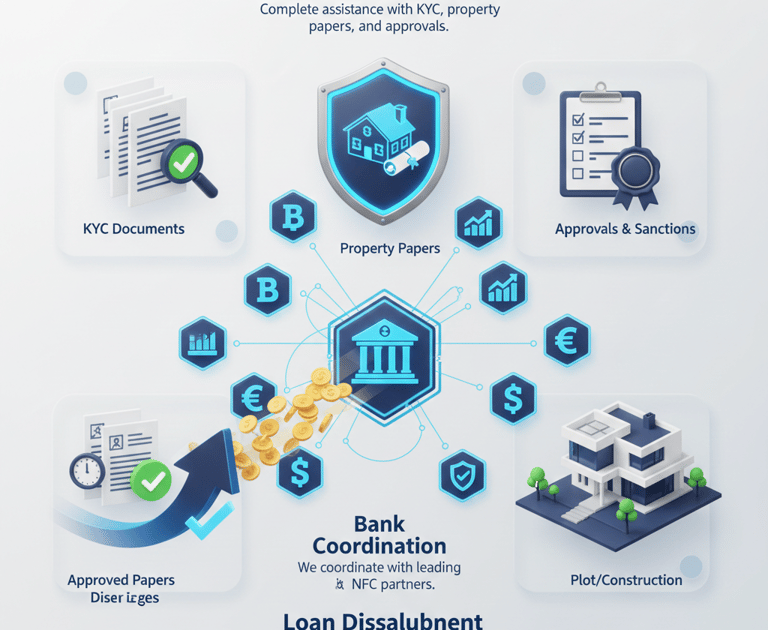

Documentation Support

Complete assistance with KYC, property papers, and approvals.

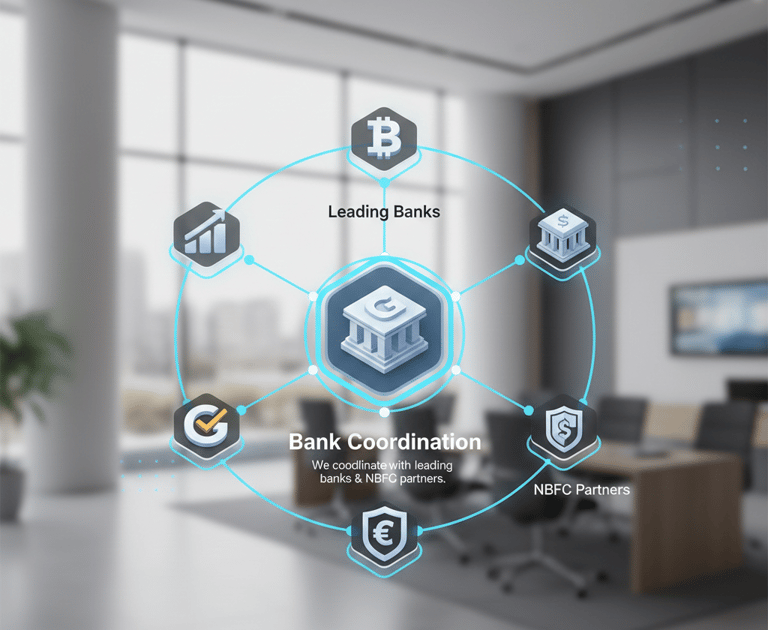

Bank Coordination

We coordinate with leading banks & NBFC partners.

Loan Disbursement

Smooth approval and timely disbursement for plot or construction.

Get Expert Home Loan Assistance

Check eligibility, compare interest rates, and get approval support within 48 hours.

Frequently asked questions

What is the minimum CIBIL score required for a home loan in Bengaluru?

Most banks and NBFCs require a CIBIL score of 700 or above to approve a home loan. A higher credit score improves your chances of getting lower interest rates and faster approval. However, eligibility also depends on income stability, employment type, existing liabilities, and property documentation.

We assist clients in assessing their credit profile before submission to reduce rejection risk.

How long does home loan approval take?

With complete documentation and pre-verification, home loan approvals can be processed within 48 hours in most cases. Final disbursement timelines may vary depending on the lender, property verification, and technical approval process.

Our structured coordination with verified banking partners helps minimize delays.

Can I get a loan for plot purchase and house construction together?

Yes. Many banks offer combined plot + construction loan options, provided the construction begins within a specified timeframe. We guide clients in structuring financing to cover both land purchase and construction costs efficiently.

Eligibility depends on property approval status and applicant income profile.

What documents are required to apply for a home loan?

Common documents required for home loan processing include:

PAN Card & Aadhaar Card

Income proof (Salary slips / IT Returns)

Bank statements (last 6 months)

Employment verification

Property documents (sale deed, approvals, layout documents)

We review all documentation before bank submission to ensure compliance and faster approval.

What is the maximum home loan tenure available?

Most lending institutions offer flexible repayment tenure up to 25 years, depending on applicant age and eligibility. A longer tenure reduces monthly EMI burden but increases total interest payable.

We help clients choose the most suitable tenure based on repayment capacity.

What interest rates are available for home loans?

Interest rates vary based on credit profile, loan amount, and lender policies. Competitive home loan interest rates may start from 7.05% onward, subject to eligibility and market conditions.

Our partnerships with leading banks and finance institutions help clients access competitive rate options.

Are there any hidden charges in home loan processing?

No. We ensure complete transparency regarding processing fees, legal charges, valuation charges, and interest rates before submission. Clients are informed of all applicable costs to avoid unexpected expenses.

What is the processing fee for a home loan?

Processing fees vary between lenders and typically range between 0.25% to 1% of the loan amount, depending on loan type and institution policies. Some lenders offer promotional waivers.

We help compare lender options for cost-effective processing.

Can self-employed individuals apply for a home loan?

Yes. Self-employed professionals and business owners can apply by providing:

Income Tax Returns

Profit & Loss statements

Business proof

Bank statements

Eligibility is evaluated based on income consistency and financial records.